FTAV’s further reading

Author: business

-

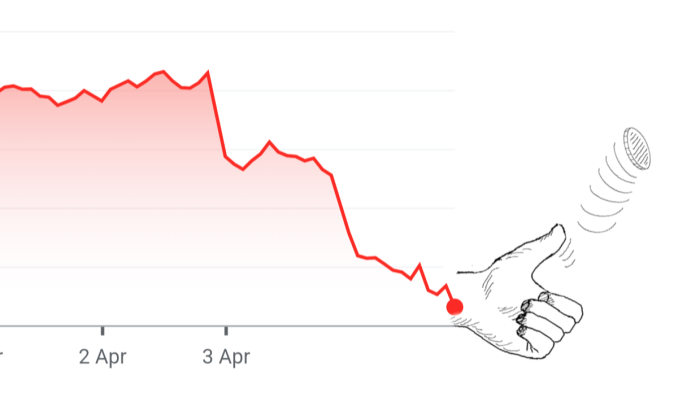

The S&P 500’s latest ‘Black Monday’ in one chart

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

You’ve consumed financial media (social, antisocial or otherwise) over the past day and a half, and you’ve encountered the phrase “Black Monday”.

Yesterday was, admittedly, a pretty wild time. But the S&P 500 closed pretty much flat, so everything must actually be fine.

Addicted to charting, we decided to raid Bloomberg’s historic open/high/low/close data for the S&P 500, and figure out just how “black” yesterday was on the Black Monday scales (we are already sure it was a Monday).

We didn’t just want to chart the day change; we also wanted to reflect some of the severe, start-of-week, intraday crapping-out that feels bad at the time but may not end up in the closing price.

So, for every Monday the S&P 500 has traded on since 1982* we compared the end-of-day loss with the maximum intraday trough, and scaled the dots based on the spread between the intraday peak and trough to capture a bit of swang. We’ve highlighted those days listed by veritable organ Wikipedia as a stock market Black Monday.

And, unsurprisingly, even with these tweaks there’s still only one real Black Monday from an S&P 500 perspective. Out in a zone of its own, 19 October 1987 remains a Monday like no other:

*

— Why does Wikipedia list the 16 September 2019 repo brouhaha as a Black Monday?

— For a smattering of days in the 1970s and early 1980s, Bloomberg lists the same price for open, high, low and close. We dunno what’s going on there, but that’s why our chart starts in 1982. Sourcing data remains hard.Further listening:

— Cypress Hill’s Black Sunday -

Avoiding Kindleberger’s Trap

Bob McCauley is a non-resident senior fellow at Boston University’s Global Development Policy Center and associate of the faculty of history at the University of Oxford.

Kindleberger’s Trap is the danger that a fading hegemon lacks the ability but the ascendant one lacks the will to supply the world economy with vital public goods — such as a reserve currency. In the 1930s, the Bank of England lacked the ability to continue to serve as international lender of last resort, and the ascendant Federal Reserve lacked the will to do so.

As a result, crisis spread from Austria to Germany and Britain and ultimately reached the US, turning the post-1929 slump into an era-defining economic collapse. The Kindleberger Trap led to “the world in depression”, as Charles Kindleberger titled his seminal book.

This is why worries over whether the Federal Reserve will continue to supply dollars to overseas central banks at times of financial strife are such a big deal. As Reuters reported last month:

Some European central banking and supervisory officials are questioning whether they can still rely on the U.S. Federal Reserve to provide dollar funding in times of market stress, six people familiar with the matter said, casting some doubt over what has been a bedrock of financial stability.

The sources told Reuters they consider it highly unlikely the Fed would not honour its funding backstops — and the U.S. central bank itself has given no signals to suggest that.

But the European officials have held informal discussions about this possibility — which Reuters is reporting for the first time — because their trust in the United States government has been shaken by some of the Trump administration’s policies.

These concerns are warranted, both in light of the Trump administration’s distaste for America’s traditional alliances and the centrality of the Fed’s swap lines to global financial stability.

As Deutsche Bank’s chief FX strategist George Saravelos highlighted in a recent report on the topic, doubts over the Fed’s willingness or ability to step up when needed is a “nuclear button” for the dollar’s future:

Ultimately, a withdrawal of the Fed as the international lender of last resort is equivalent to a suspension of the dollar’s role as the safest of global currencies. Doubts about a commitment from the Fed to maintain dollar liquidity — especially against major allies — would accelerate efforts by other countries to reduce their dependence on the US financial system. It would ultimately lead to lower foreign ownership of US assets and a broad-based weakening of the dollar’s role in the global financial system.

In the 2008 and 2020 dollar panics, the Fed wisely told 14 central banks that the buck starts here. Through official swap lines the Fed could extend its credit to each central bank against domestic currency as collateral. Each central bank could in turn lend the dollars to banks in its market against domestic collateral.

Reaching outstandings as high as $598bn in 2008 and $449bn in 2020, the swaps succeeded in stabilising global dollar markets. The amounts were not small, but offshore dollar lending — both on- and off-balance sheet — is measured in the tens of trillions of dollars. Thus, with pennies on the dollar lent and repaid with interest, co-operating central banks calmed these potentially destructive dollar panics.

The US also won from the Fed’s international provision of dollars. Crucially, the swaps reversed market-driven interest rate hikes on Libor-priced US corporate loans and mortgages, which in turn would have hammered US jobs and consumption. As Saravelos pointed out:

Had the Fed not stepped in during the 2008/9 financial crisis and Covid pandemic, the reserves of foreign central banks and international lenders like the IMF would unlikely have been sufficient to meet global dollar demand, leading to an even greater surge in dollar borrowing costs than occurred at the time, defaults, and potentially systemic implications for the global financial system.

What if a crisis like 2008 or 2020 happens and the Fed does not swap dollars? Central bankers would not be doing their jobs if they weren’t asking this question.

If it came to such a scenario of “politicise[d] . . . recourse to the dollar swap lines,“ the Fed would have the ability but not the will, as in 1931. Any other single central bank might have the will but not the ability.

However, central bankers could form a dollar coalition of the willing.

The central fact is that the 14 central banks that had standing and temporary Fed swaps in 2008 and 2020 collectively hold lots of dollars. Their collective holdings of US safe assets amounted to an estimated $1.9tn at the end of 2021. (Their total foreign exchange reserves at the end of 2024 were about double that sum.) That $1.9tn is big money. It’s triple the previous maximum drawing on the Fed swap lines in 2008, and four times larger than the peak 2020 usage.

© Deutsche Bank Leadership could arise among the Fed’s standing swap partners, the European Central Bank, Bank of Japan, Swiss National Bank, Bank of England, and Bank of Canada. The ECB and BoJ were the largest users of the Fed swap lines in 2008 and 2020, respectively. During the 2023 run on Credit Suisse, the SNB acquired unique experience in tapping the New York Fed for $60bn against US Treasury collateral under the FIMA (foreign and international monetary authorities) repo facility.

The coalition could enlist the Bank for International Settlements for technical support as agent as European central banks did in 1973-95. Or the BIS could serve as intermediary, as it did when the New York Fed lent dollars through the BIS to offshore banks in the 1960s to prevent funding crunches.

However, there is a major wrinkle: the $1.9tn is invested, and a crisis calls for cash dollars. In a world where the Federal Reserve refuses to allow access to its swap lines, would the New York Fed continue to provide same-day FIMA repo funding against Treasuries held in custody?

If it did, the coalition could arrange to access hundreds of billions of dollars in same-day funds. If the Fed did not, then it would end up providing ad hoc funding.

Without the FIMA backstop, heavy central bank sales of US Treasuries would rock the US bond market. Such selling could prod the Fed into the market as buyer of last resort — as in March 2020, before the FIMA repo was introduced.

Without the FIMA backstop, the Fed similarly would have to cap market repo rates if central banks sought to repo Treasuries for cash in size. However, the recent benchmark rate shift from dollar Libor to repo-based Sofer means that the Fed’s own domestic monetary transmission requires well-behaved repo rates.

One way or another, the coalition would need to work with the Fed to manage any “dash for cash.” Even a large pool of dollar reserves would not stack up to “whatever it takes” Fed swaps. Limits excite. It may be, as Eurosystem sources grimly noted to Reuters, that “there is no good substitute to the Fed.”

Nonetheless, a dollar coalition of the willing could pool trillions of dollars to backstop global dollar funding with no more than self-interested Fed help. An inferior lender of last resort beats no lender of last resort.

-

It’s possible that Pink broke UK hotel inflation. Has the ONS fixed it?

It was that Monday again. Shifting a plate of half-eaten toast to the edge of the kitchen table, Zoë checked her list and started making calls.

They answered on the seventh ring.

“Hello, Travelodge Telford.”

“Hello,” said Zoë, slipping into the ‘work voice’ her housemates always teased her over. “I’m calling to inquire abo—”

“That time again is it?” the receptionist cut her off, in a voice that was neither cruel nor particularly cheerful.

“Time is absolutely flying,” said Zoë.

“Right,” he replied. “Well, we have a room tomorrow. One night with breakfast, £35.15. Do you want me to book that for you?”

“No,” said Zoë. “Of course I don’t.”

Swift justice

We made Zoë up. But her story could be true.

Every month, during the Monday of “index week”, agents of the Office for National Statistics like our fictional heroine are tasked with collecting a range of hotel prices.

Over the internet or via old-fashioned phone calls, they trawl hotels to discover the cost of one night in room with breakfast for Tuesday. The prices they observe will form a small part of the inflation basket, which will mostly be filled over that next day.

In the latest consumer price index figures, this “Hotel 1 Night Price” item was weighted at about 0.3 per cent of the overall basket — higher than water and wine, but behind vodka and pub meals.

Usually, it isn’t a big deal, but that changed last summer, around the same time a global obsession with pop star Taylor Swift led to the ‘Me!’ singer suddenly being credited with just about everything happening in the economy:

FT Alphaville wrote a couple of times last summer about how a jump in ONS-imputed hotel prices during June was likely not the work of Miss Americana.

Our crucial point, insofar as we had a point, was that even if Swift’s appearances did lead to hotel price gouging, that gouging would not have matter from a national statistics perspective unless her appearances coincided with ONS price collection days. Which they didn’t:

So if the ONS was missing Swift, what were they capturing? Well, as it turns out, there a large number of other musical acts who are also popular.

Missundaztood

Alecia Moore-Hart is probably not a household name in the UK, but her stage name, Pink (often styled as P!nk), certainly is.

The “Just Like A Pill” singer’s Summer Carnival tour ran for 97 shows, from summer 2023 to autumn of last year. According to Billboard, it was the second-highest-grossing tour by a female artist ever, landing ahead of Beyoncé’s Renaissance, and behind — you guessed it — Swift’s Eras.

Among a number of appearances across the British Isles, she appeared at Cardiff’s Principality Stadium on 11 June, bulls-eyeing the price collection day for that month:

If a hotel in Cardiff increased its prices on the night of the 11th in response to high demand linked to Pink’s appearance, there’s a possibility that could then feed into the UK’s inflation data.

Now, we can’t see specific figures for Cardiff, but the ONS’s price quote tables do show agents’ attempted observations for Wales as a whole. How many hotels did they canvass that June?

Four. Four hotels across Wales, a country of around 3 million people and home to, uh, the ONS.

Of those four hotels, two produced a price: one of £57 for the night, and one of £369. The other two got a T indicator, for “Temporarily out of stock” — in other words, the hotel was fully booked.

The £57 room’s price was flat on the previous reading, while the £369 room’s price had almost tripled:

You probably don’t have to be a sell-side economist to work out why that chart is bad. As of last June, Welsh hotels represented 5.67 per cent of the “Hotel 1 Night” item. Alongside some other individual surges in the South West and East Anglia, this hotel was probably a major driver of inflation in broader category.

This Pinkcident was brought to our attention Rob Wood from Pantheon Macroeconomics, who noticed it at the time and mentioned it to us while we were nagging him about video games last week.

It’s a clear example of how easily Hotel 1 Night Stay can be skewed, and then how that potentially feeds up to headline numbers.

The ‘no room at the inn’ issue

Like many works of fiction, our short story at the top of this article included an improbable event: Zoë managed to find a room.

It’s probably a little tricky to eyeball this from the chart above, so let’s specifically look at the number of valid Welsh hotel price quotes the ONS’s agents have been able to get each month since 2019. It’s, uh, horrible:

So, out of the seven hotels it has tried to get prices from since September 2019, the ONS have never successfully extracted a valid price from more than four.

Even if we ignore the lockdown-era disruption, the change in price has frequently been derived from a single hotel price, or none at all — as was the case in the most recent figures.

It doesn’t much imagine to guess why this might be happening: if you try to book a hotel room the day before you plan to arrive, you’re often going to find that they’re full. You’re also going to end up in a weird valley regarding dynamic pricing: sometimes, you’re begging for a gouging, while other times the hotel might be desperate to fill a room.

And it’s not just a problem in Wales:

And unlike with video games, there’s no major apparent shift in the style or amount of gathering going on here:

An ONS spokesperson told us:

The observation for the traditional overnight hotel accommodation is as described. The price is collected on the Monday of collection week for an overnight stay the following day. This can mean that some accommodation is fully booked and prices can be affected by short-term demand.

So what?

It isn’t good for the stats beneath the stats to be this bad. And unlike with an innocent small caged mammal, hotels are significant enough to sometimes matter a bit to overall CPI.

Not all items are alike. But, as we observed long ago, price collection rates (successful or not) are radically different for different items. Under ideal circumstances, you’d hope that the more important the item to overall, the more the ONS is trying to measure it.

Lol, nope:

Much to consider.

So what’s the solution? We already know the ONS is slowly attempting to make tweaks, most significantly by mass price gathering from sources like supermarket scanners.

Hotels don’t seem to be getting the big data treatment just yet, but, happily, a fix of sorts is in: we’d like to be among the first to congratulate the ONS on its new inflation spawn, HOTEL ADVANCE PRICE 1 NIGHT. We don’t appear to have price quotes for this beautiful new baby in a basket, added in February, but hope to see some soon.

An ONS spokesperson told us:

As part of the latest basket update, we have added an extra item to cover overnight hotel accommodation booked further in advance. This will result in additional quotes and should reduce the volatility in the series, aiding interpretation. We are also retaining the existing item so that late-booked accommodation is represented.

Huzzah! Still, our national statistics are going to occasionally going to be victim to strange circumstances. And we’re happy to give Pink long-overdue props for her part in that.

Further reading:

— The ONS vs the Xbox -

Did an anonymous X account send markets reeling today?

Monday’s trading action was bizarre in many ways.

But one specific mystery — about a misleading headline that sent stocks ping-ponging all over the place — highlights just how fragmented and expensive access to breaking financial news can be, even at times when it really matters to retail investors.

The US stock market did indeed go bananas this morning, thanks to a headline that falsely* claimed White House adviser Kevin Hassett had said President Donald Trump was considering a 90-day pause in tariffs.

CNBC anchors read out the headline on air, as they tried to explain why markets had started to soar. In all, the S&P 500 rallied nearly 6 per cent from where it had been trading right before the mystery headline.

The White House said within the hour that no one knew about this supposed plan, a rare chance to properly use the term “Fake News”. Stocks sold off by the same amount they’d rallied, and then see-sawed around for a while. By mid-afternoon they were basically flat for the day.

So where exactly did the headline come from? That’s a much tougher question to answer than you’d think.

The obvious point of contagion was the Walter Bloomberg account, using the X handle @DeItaone (with a capital I instead of an “L”) which says it’s based in Switzerland.

This is not a guy named Walter Bloomberg, nor does he write for Bloomberg. The account’s entire deal is just reposting financial newswire headlines.

Here’s the post via a screengrab (since the account has since deleted the post). As you can see, it came at 10:13am, and really made the rounds within the next 30 minutes or so, thanks to the account’s ~848,000 followers:

© Apologies, we cannot remember where we got this screengrab from. This reporter was on the phone until 10:45 and then had to catch up fast. By the way, all the times we’ll mention are EDT since the action happened during the New York trading day.

So did someone posting as “Walter Bloomberg” make up a headline to save the market? To cash out? Or just to introduce some chaos into the day?

If so, it’d be strange for the account to keep posting! But it has.

When asked by followers, the Walter Bloomberg account cited both Reuters and CNBC as the sources of the headline. Remember, though, the CNBC anchors seemed to be reading his post! One of his screengrabbed sources shows a Reuters newswire headline. But that was from 10:23am, and cites CNBC:

— *Walter Bloomberg (@DeItaone) April 7, 2025

Now, it’s not great if CNBC flashed a headline because one of their anchors read a social-media post that turned out to be nonsense. In their defence, however, markets had already started to take off before they read it!

But is the lesson here really just that the @DeItaone account has massive influence?

Probably not! Things get weirder from here.

An account called Hammer Capital posted the same headline at 10:11am. That’s before the post from Walter Bloomberg, or CNBC, or any other sources we’ve found. Hammer Capital, who has been on X since March 2021, explained the headline thusly:

To be as abundantly clear as possible, trading desks started sending out this headline at 10:09.

I was regurgitating what the market was reacting to, to my 600 followers.

It was an incorrect interpretation of a Fox News interview. https://t.co/RpN6c5RqfW

— Hammer Capital (@yourfavorito) April 7, 2025

We’ve heard from few other sources now that trading desks started sending around that headline around at that time. We’ve contacted both accounts we’ve mentioned for additional comment.

Also, looking at the not-so-sophisticated trading data this writer has available at home, S&P 500 futures trading volume surged around then, before the Walter Bloomberg or Hammer Capital tweets were posted.

So . . . where did the banks get the headline?

As we said, the “Walter Bloomberg” account basically just copies financial breaking-news headlines from newswires. And the thing is, those wires often come with an extremely pricey subscription. If Hassett had done an exclusive interview about major US policy decisions — and he did not, probably* — only a major financial news service would’ve been able get that exclusive access.

The newswires don’t just offer one uniform news feed, either. While we aren’t 100% up to speed on the latest business models, some newswires have been known to deliver news feeds to different subscribers at different speeds. This is reasonable, to an extent, because not all professional subscribers can use the same level of access.

So it seems possible that some experimental headline-writing product (or a budget subscription) published a bad headline that was then picked up by the Walter Bloomberg account.

There’s one less-than-obvious analogue with reality, which could have been misinterpreted by an overzealous headline writer or (ahem) an LLM. In a Fox & Friends interview, National Economic Council director Kevin Hassett stalled by saying “yep” before saying “the President is going to decide what the President is going to decide.”

This was obviously not confirmation, because he then argued that observers are overreacting to the tariffs news.

Another problem with that explanation is that the interview happened nearly two hours before @DeItaone published the headline. And Hassett’s ‘Fox & Friends’ comments wouldn’t have explained the part about an exception for China. Reuters provided the following comment to FT Alphaville:

Reuters, drawing from a headline on CNBC, published a story on April 7 saying White House economic adviser Kevin Hassett had said that President Donald Trump was considering a 90-day tariff pause on all countries except China. The White House denied the report. Reuters has withdrawn the incorrect report and regrets its error.

So they’re pointing the finger at CNBC. But again, the network’s anchors seemed as confused as anyone else by the rally and the accompanying surge in trading volume when it first happened. (We’ve seen the video!)

And from CNBC:

As we were chasing the news of the market moves in real-time, we aired unconfirmed information in a banner. Our reporters quickly made a correction on air.

We’ll see what we can find out about where banks’ trading desks and broker chats saw the original headline.

Anyway, the market zigzagged all over the place after the morning ruckus, and closed basically flat. That’s presumably because some traders think the US President can be swayed by market reactions to fake news.

Or, as the @Quantian account puts it:

So we bounced 8% on a fake headline, sold off when people realized it was fake, and then bounced again when it occurred to people that if we bounced that much on a fake headline imagine how much we’d bounce on a hypothetical real one.

*The original headline’s accuracy could, of course, change entirely at any moment, at the whims of one man. How fun! Also an earlier version of this headline said Twitter instead of X. Whoops.

-

Goldman Sachs sees US recession if full tariffs go into effect

Stay informed with free updates

Simply sign up to the Global Economy myFT Digest — delivered directly to your inbox.

Within an otherwise anodyne note from Goldman Sachs assigning a 45-per-cent chance to a recession, readers can find the following paragraph (with our emphasis):

If most of the April 9 tariffs do take effect, then the effective tariff rate will rise by an estimated 20pp once those increases and likely sectoral tariffs take effect, even allowing for some country-specific agreements at a later date. If so, we expect to change our forecast to a recession.

Doesn’t get much simpler than that!

The funny thing is, GS’s house view is still a ~15-percentage-point increase in tariffs on Wednesday, not the ~20-percentage-point one that was announced.

And even then, the bank sees greater recession risk than there was one week ago.

In other words, even if there is a rollback, it’ll be harder to shake the decline in confidence, and the very real fact that the US has now pissed off a ton of its major trading partners.

The bank puts it more mildly, citing a greater “sensitivity of financial conditions to incremental tariffs”, including the 34-per-cent retaliatory tariffs that China imposed on the US late last week.

It also cited the ongoing “sharp tightening in financial conditions” (ie stocks sold off), along with “foreign consumer boycotts, and a continued spike in policy uncertainty that is likely to depress capital spending by more than we had previously assumed.”

They cite the decline in travel and warn about consumer boycotts, which all seem very possible:

It also seems likely that the US’s habit of detaining foreign travelers for no apparent reason has contributed to the drop in tourism as well. Not to mention disappearing non-citizens for having tattoos, or for simply exercising their First Amendment rights.

Anyway, if there’s no recession and the tariffs are rolled back to just a 15-percentage-point increase, GS still expects three “insurance cuts” from the Fed this year.

If the tariffs do go into place on April 9, the economists at GS expect the Fed to cut around 2 percentage points over the next year. So cheaper mortgages, but also a recession . . . Quite the trade-off!

-

So much winning — in 15 charts

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

You might have missed it, but April is “Financial Literacy Month” in the US. On April 1 (yes, really!) the White House released the following statement from Donald Trump:

During this National Financial Literacy Month, I urge families, communities, schools, and institutions to commit to bolstering their financial knowledge. There are amazing resources available to you and your family through the Department of the Treasury’s website that will assist you in making sound financial decisions. Together, we can all protect each American’s right to economic freedom, securing the promise of prosperity for generations to come.

Kudos to the White House for all all-time classic April Fool’s joke, and H/T Richard Metcalf for the spot. Anyway, here’s a selection of charts pilfered from various sell-side research notes that show how the US government’s sound financial decisions are securing the promise of prosperity for generations to come.

Tariffs up (zoomable image):

© JPMorgan Stocks down (zoomable image):

© Deutsche Bank Credit also clobbered (zoomable image):

© Deutsche Bank Bigly moves pretty much everywhere (zoomable image):

© Goldman Sachs Yet 10-year Treasury yield only down by 25 bps (zoomable image):

© Deutsche Bank First-quarter earnings expectations fading (zoomable image):

© Barclays Equity volatility up (zoomable image):

© Deutsche Bank Uncertainty up (zoomable image):

© Goldman Sachs Inflationary pressures climbing (zoomable version):

© Apollo Unemployment expectations rising (zoomable version):

© Goldman Sachs Business confidence down (zoomable image):

© Goldman Sachs Bankruptcies already rising (zoomable image):

© Apollo The GDP impact of tariffs (zoomable image):

© Principal Asset Management Lots of rate cuts getting priced in (zoomable image):

© JPMorgan But recession expectations still climbing (zoomable image):

© Goldman Sachs Further reading:

— Global stocks tumble as Donald Trump offers no respite from tariffs (FT) -

How imported eggs saved American breakfast

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Before roiling global markets with his tariff plan last week, US President Donald Trump took a few moments to tout a decline in the price of eggs.

There was a very deep irony to this. Inflation in egg prices and other household staples probably contributed to his win. And for eggs specifically, the recent drop in prices was fueled by a yuge jump in imports.

In other words, America’s protectionist President imposed a set of baffling tariffs, targeted to reduce bilateral trade deficits, while trumpeting a price drop driven by two key trading partners.

The plan to import eggs was no secret during the peak of the price spike and shortages, when even Waffle House had to tap out. And to be fair, agricultural commodities aren’t what drive the biggest trade imbalances with the US, because they are often outstripped by electronics, other big-ticket items, or geographically-concentrated industries like textiles.

But it’s still an illustrative reminder of why trade can be useful. And we can now see it in more detail, thanks to data published late last week by the Census Bureau and USDA.

Two countries stepped into the birdflu breach in February: Turkey and Mexico. They exported more than four times as many eggs that month as they did the prior year, according to the USDA.

From the USDA’s latest weekly egg-market report, published Friday (with our emphasis):

Overall imports of shell and egg products exploded in February as the domestic market sought relief from reduced production resulting from persistent outbreaks of highly pathogenic avian influenza in the first two months of the year.

Overall volume was up 551 percent; 404 percent over a year ago. The overall value of imports was similarly higher, up 328 percent for the month and 450 percent for the year. Imports of table shell eggs increased 478 percent with Turkey and Mexico contributing at a 60/40 split. Imports of liquid egg products were down 13 percent for the month but 43 percent over year ago levels. Imports of liquid whole egg were down 15 percent as shipments from Vietnam slowed. While imports of liquid yolk declined 33 percent as trade with Canada slowed. Only liquid albumen posted an increase, up 30 percent and all from Canada.

There’s a real lesson here, we think. Plenty of ink has been spilled already about how trade provides commodities that a country doesn’t have (eg diamonds or bananas).

This shows that trade also can protect from supply shocks in commodities and goods a country does have. Like, say, an outbreak of disease. One can argue about how much the price pinch was exacerbated by issues besides bird flu — like monopoly power and factory farming — but $8 for a dozen eggs is inarguably rough maths!

On the bright side, the US has only imposed a 10-per-cent tariff on Turkey because it had a relatively small trade deficit with the country (around 9 per cent) in 2024.

As for Mexico, it isn’t entirely clear whether egg imports from Mexico are all considered compliant with the USMCA. If they are, they would dodge all tariffs under the new regime. But Mexico only provided a small portion of the eggs that the US was importing.

Next outbreak, the US will simply have to ask skincare brand The Ordinary to start egg pop-up sales all over the US.

Another bit of irony: that company is based in Canada, which imported nearly $97mn of eggs from the US in January and February.

-

America’s endangered ‘exorbitant privilege’

Stay informed with free updates

Simply sign up to the US economy myFT Digest — delivered directly to your inbox.

The stock market car crash is naturally dominating attention. After all, this is only the fourth two-day 10 per cent decline since at least 1952. But the more alarming developments are happening in currency markets.

The DXY dollar index has bounced a little today, but the growing sense of unease about its trajectory is nearly palpable. Yesterday, we wrote of Deutsche Bank’s concerns that we should “beware a dollar confidence crisis”, and this morning Société Générale sounded a similarly dour now.

As SocGen’s chief FX strategist Kit Juckes pointed out earlier today, the US dollar’s exceptionalism has been powered by gargantuan inflows of foreign money over many many decades. “That money is thinking about packing its bags and heading somewhere else,” he warned.

The BEA puts the end-2024 US net international investment deficit at USD 26.2 trn (and the sum of assets and liabilities at USD 88trn). Anything that scares foreign investors away from US assets can have a bigger negative impact on the dollar than a shift (even a sizeable one) in the price of import and exports.

However, it’s not just European strategists at European banks dissing the American dollar. Goldman Sachs’ FX team are out with a new call this evening, and it’s a big one. They now see the US dollar’s weakness “persisting and deepening further”.

The trigger is not, per se, the extreme level of the “reciprocal” tariffs that the Trump administration rolled out this week, which they say were incorporated in its previous forecasts. Goldman’s changing view has more to do with its sharp reappraisal for what the new regime means for the dollar.

Like many other analysts, Goldman’s previously reckoned that tariffs would buoy the dollar. Now it thinks otherwise, “for a number of reasons”. Alphaville’s emphasis below:

First, the combination of an unnecessary trade war and other uncertainty raising policies is severely eroding consumer and business confidence . . . so that any Dollar positive impulses are being offset by the likelihood of lower growth.

Second, the negative trends in US governance and institutions are eroding the exorbitant privilege long-enjoyed by US assets, and that is weighing on US asset returns and the Dollar, and may continue to do so in the future unless reversed.

Third, and related, the implementation of the tariffs themselves is eroding the ability of investors to price these. While it is still true that currencies (and Dollar strength) provide the most natural margin of adjustment to US tariffs, as was the case both in the first trade war and also in the first episode of Canada/Mexico tariffs in late-Jan/early-Feb, the constant back and forth on timelines and the rudimentary calculations compound the uncertainty that underpins rising recession risks.

Moreover rather than clearly targeted tariffs that allow precise room for negotiation, with such broad, unilateral tariffs there is less incentive for foreign producers to provide any accommodation — US businesses and consumers become the price-takers, and it is the Dollar that needs to weaken to adjust if supply chains and/or consumers are relatively inelastic in the short term.

The upshot is that Goldman’s new base case is now the dollar’s “exceptional” position over the past decade is now reversing, which will benefit the euro and the Japanese yen in particular.

In forecasting terms that means the EUR/USD exchange rate will go to to 1.12, 1.15 and 1.20 over the next three, six and 12 months (from 1.07, 1.05 and 1.02 previously) while USD/JPY will go to 138, 136, and 135 in three, six and 12 months (from 150, 151 and 152 previously)

However, the most interesting part of the note is that even Goldman Sachs is becoming worried that the sun may finally be setting on America’s famous “exorbitant privilege” (and is willing to say so publicly).

That might be a little premature, but we can begin to freak out if we ever see multiple days of US Treasury yields rising and the dollar falling in tandem. That would be a pretty clear sign that some of that $26tn NIIP is truly heading for the exit.